Grow Your Business

Grow Your BusinessWhat you need to know about credit card processing.

One of the most important decisions that you’ll make as a new business owner is choosing how you’ll accept payments. There are options when it comes to credit card processors (also called merchant account providers) that are definitely worth considering. Here at BankCard USA, we want to provide you with the information you need for choosing the right credit card processor for your business.

There are thousands of credit card processors registered with Visa, Mastercard, American Express and Discover. Their primary focus is to collect customers’ money and pass it to the businesses they work with. Processing these transactions is done on a very large scale by several credit card process networks. These include First Data, Paymentech and Global Payments. These companies sell access to their networks on a wholesale basis to other companies that resell them under their own brand. These include big banks such as Bank of America and Citibank. They bundle these services with other merchant services for their business clients. There are also smaller credit card processors that offer more tailored services to their clients.

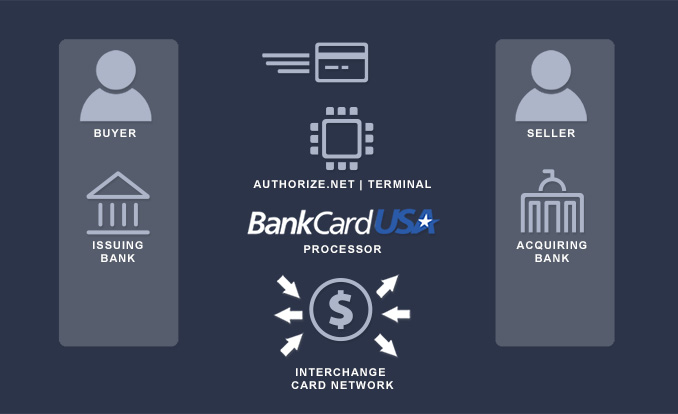

Step 1. The customer submits his/her credit card for payment.

Step 2. Authorize.Net manages the complex routing of the data on behalf of the merchant through the following steps/entities.

Step 3. Authorize.Net passes the secure transaction information via a secure connection to the Processor. The Merchant Bank’s Processor submits the transaction to the credit card network (like Visa or MasterCard). The credit card network routes the transaction to the bank that issued the credit card to the customer.

Step 4. The issuing bank approves or declines the transaction based on the customer’s available funds and passes the transaction results back to the credit card network. The credit card network relays the transaction results to the merchant bank’s processor. The processor relays the transaction results to Authorize.Net.

Step 5. Authorize.Net stores the transaction results and sends them to the website for the customer and merchant to see.

Step 6. The merchant delivers goods or services to the buyer.

Step 7. The issuing bank sends the appropriate funds for the transaction to the credit card network, which passes the funds to the merchant’s bank. The bank then deposits the funds into the merchant’s bank account. This is called “settlement,” and typically the transaction funds are deposited into the merchant’s primary bank account within one to two business days.

There are three types of fees associated with processing credit card transactions:

Are you ready to find the right credit card processor for your business? Great! You will probably want to gather information from a variety of sources including:

Pricing for credit card processing can be confusing. Pricing structures differ widely which makes it challenging to compare quotes. With that said, there are four pricing structures or ways that rates are typically quoted:

This is the most straightforward form of pricing because you can clearly assess total fees that include interchange, assessments and processor markup. Most businesses prefer this option because it is the most transparent.

2. Tiered Pricing

Tiered pricing is another common form of pricing that groups transactions together into tiers with differentiating rates. Often, processors will quote pricing from the lowest tier to entice businesses with low rates. However, rates for other tiers are often significantly higher. These higher rates are often not clear upfront and hidden in fine print. In almost all cases, tiered pricing is not going to be your best option.

3. Enhanced Reduced Recovery (ERR) or enhanced billback

With ERR, the credit card processor quotes a single rate for every transaction. But, there are often hidden fees for certain categories of cards, such as business and reward cards.

4. Fixed Rate Pricing

This is the most basic type of credit card processor pricing option, and the best option for many small businesses. The fixed pricing is structured with a percentage-based and per-item for all transactions, and usually the rate is reasonable.

There are similarities between interchange plus pricing and tiered pricing, and they can even be confused. However, it’s important to take the time to determine what you’re really looking at when you receive a quote from a credit card processor.

Are you more confused than ever? Don’t be. There are a few simple strategies for finding the right credit card processor for your business.

Of course, you need more than just a credit card processor to take customer payments. You’ll also need some specific tools depending on the type of business you have.

A terminal is the piece of equipment you see on a retail store’s counter to swipe a credit card. The information collected from a terminal is encoded and passed on to your credit card processor safely and quickly. In almost all cases, you will not need to purchase a new terminal if you switch processors. They can typically be reprogrammed by your new processor.

A gateway refers to the software that transports the credit card information from your customers (either collected on your website or a virtual terminal) to your credit card processor. If you sell online, you will definitely need a gateway, as well as a credit card processor. The gateway is what sits between your shopping cart software and your credit card processor.

Authorize.net is the most widely used gateway, but some processors and resellers have their own gateways that they offer—sometimes at below-market pricing. These captive gateways can be acceptable for most businesses. However, there can be challenges down the road when you want to switch processors.

A “point of sale” system is a terminal that has more features and functionality for a business. This computerized solution connects through the gateway and can collect data on purchases and generate reports. Often times, POS systems are specific to an industry such as to restaurants or retail.

While we’ve already touched on the basics of credit card processors, there are some other commonly used terms that are worth familiarizing yourself with.

Third party processors serve as both gateways and processors for online payments. The most popular of these processors are PayPal, Google Checkout and 2CO.

For very small businesses with monthly revenue under $5,000 per month, they are often the cheapest solution because they have such a low setup fee and a fixed pricing model. Once you grow, it pays to look elsewhere because third party processor fees can be as high as 5.5% per transaction.

It’s also important to note that when you use a third party processor, their name will show up on customer statements instead of your business. This can be confusing to your customers and can lead to potential chargebacks.

A chargeback is when a customer disputes a charge that appears on their bill. If a merchant is unable to pay back a customer who is disputing a charge or provide them with a new product, the merchant account provider will be liable for the amount.

Credit card processors sometimes require businesses to put aside a certain amount to cover potential chargebacks. Typically, only businesses with bad credit or those in risky industries are asked to meet a reserve requirement.

PCI compliance rules are to make sure that customers’ credit card numbers are not easy to steal. Businesses must meet PCI compliance requirements. However, this is easy to achieve by simply not storing cardholder data, and letting your gateway store it instead.

Understanding the ins and outs of credit card processing can be a challenge. However, we hope we’ve provided a little insight and guidance to help you choose the right credit card processing option for your business.